Construction projects tend to use more and more mechanical construction methods to keep up with the present trend of mechanization of industries in the world.

The cost of construction equipment could be up to around 40% of the total cost of a project. A contractor may use general and specialized types of equipment to complete a construction task within the stipulated time and maintain quality.

One of the prime factors one should have in mind is to keep the estimated construction costs as low as possible. That will ultimately contribute to the profit of the project.

To calculate the unit costs of various construction tasks, it is necessary to estimate the costs of using construction equipment.

Sometimes, a contractor may hire or lease construction equipment to execute the work. The organization or individual, who hires or leases equipment will have to estimate the owning and operating costs to establish the hire rate for the plant.

Therefore, it is necessary to understand how owning and operating costs are estimated.

In the construction industry, the productivity of construction equipment is expressed on an hourly or daily basis. Therefore, the owning and operating costs of construction equipment are also estimated on an hourly or daily basis.

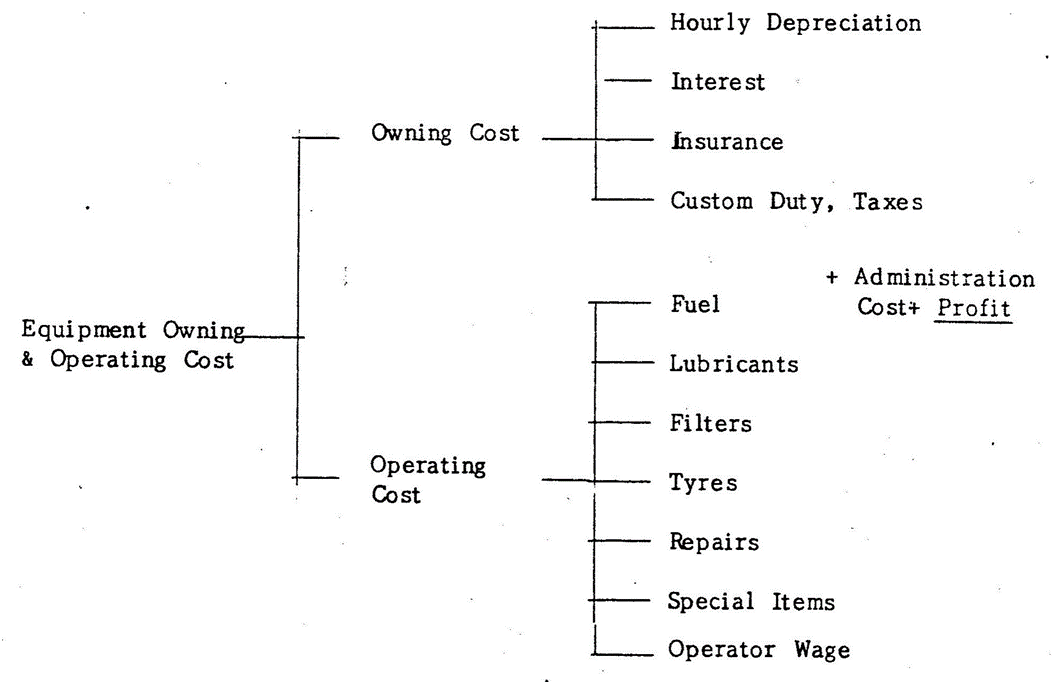

Elements of owning and operating costs of equipment

Owning Costs

These costs are also called fixed costs as these have to be incurred even when the equipment is not being operated.

The owning costs comprise the following;

- Hourly Depreciation Costs

- Interests on borrowings

- Insurance

- Custom duty, taxes, road taxes, etc.

Depreciation

Depreciation in accounting is an estimate expressed in terms of costs, of the amount of service potential of a depreciable asset that expires in a given period. The depreciation may be caused due to physical deterioration or obsolescence.

Physical deterioration results from use, wear and tear, etc. Even if a good maintenance and repair practice is in effect, equipment will have to be eventually discarded.

Obsolescence refers to when equipment becomes out of date or obsolete. An item of equipment may exist in sound physical condition, but it may be outdated as more efficient, economical, and higher-quality machines have become available.

Depreciation distributes systematically and rationally the cost of depreciable equipment less salvage value over the useful life of the equipment.

As said in the earlier statement to estimate periodic depreciation the following factors will have to be considered.

- Purchase price – may include all charges, such as duty and installations.

- Estimated salvage value – This represents how much can be recovered when this item is disposed of.

- Estimated useful life – This may be expressed in hours or years.

There are three methods of deprecation of construction equipment. They are;

- Straight line depreciation

- Double decline balance

- The Sum of years digits

In the first method of depreciation, it is considered that wear, deterioration, and obsolescence of equipment are directly proportional to elapsed time.

The second and third methods are considered to be accelerated methods where larger amounts of depreciation are recorded during the early years, than in the later years.

Interest, insurance, taxes, and duty

The item of equipment may have been purchased on a loan or leased from a bank or leasing company. Then, it is necessary to consider the interest of a loan or lease. This amount can be calculated annually. That amount can be divided by the annual estimated hours of use to find out the estimated rate per hour.

Insurance premiums can also be distributed over the estimated annual use of equipment hours.

The usage of construction plants and equipment will be the main factor that causes the expiration of assets. In this case, depreciation can be based on physical output.

The depreciation charge per unit of output may be found using the formula given below;

In this, the periodic depreciation is found by multiplying the rate per unit by the actual number of units produced during the same period.

Operating costs

These costs are proportional to the time that equipment is used for work. These costs can be categorized in to the following areas;

- Fuel

- Lubricants and grease

- Filters

- Tyres

- Repairs

- Special items

- Operator wages

Fuel

The estimated hourly cost of fuel can be found by multiplying the estimated fuel consumption by the unit cost of fuel.

Estimated cost of fuel per hour = fuel consumption per hour X unit rate

The hourly consumption of fuel can be calculated by data maintained by the equipment owner or by using the manufacturer’s data. However, construction equipment does not work under full load conditions continuously. Therefore, a load factor should be used to correct the consumption of fuel at load.

Consumption of fuel under job condition = consumption of fuel X load factor fuel under full load

However, the reliable method of calculating the fuel consumption is by direct observation under site conditions.

Lubricants and Grease

The requirement for lubricating oil and grease will vary with the type of equipment. During the early days, only engine oil, gear oil, and grease were used in construction equipment. Today, most of the construction equipment uses hydraulic systems. Therefore, the need has arisen to estimate the requirement of hydraulic oil in addition to the above-mentioned lubricants.

Approximately, this could be taken as 10% of the cost of fuel.

Filters

The filter costs may be calculated using the formula given below;

Tyres

The replacement cost of tyres accounts for a reasonable percentage of the purchase price of wheeled equipment. Therefore, the hourly tyre costs are estimated separately.

The tyre life will depend upon factors like surface conditions, operating speeds, the position of the wheel – driving or trailing, loaded, curves on haul roads, grades on haul roads, etc.

Repairs

Repairs represent a considerable amount of the operating cost of equipment.

The repair costs are low during the initial period and rise gradually towards the end period of estimated life. If one is to consider the repair cost properly it will be an increasing item increasing along with life. To avoid that this can be averaged from the first hour of use of equipment till the last hour of estimated use.

So, if records are maintained concerning repairs, one could see that during the initial period, money is being lifted out of the estimated repair cost. It is sometimes called a repair reserve also.

Generally, the cost of repairs is again estimated using factors that will vary with the job conditions.

The estimated repair cost will be equal to;

Estimated hourly repair cost = Repair factor X Hourly depreciation cost

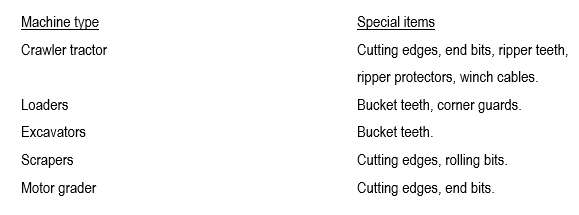

Special items

Construction equipment may be fitted with various special items used for digging, scraping works, etc. The following list gives types of special items that could be fitted onto construction equipment by machine type.

The cost of special items per hour can be calculated using the following formula.

Operator wages

The operator’s wages also can be taken into consideration.

Administration cost

These are also called overhead expenditures, such as;

- Establishment costs of the organization,

- Recurrent expenditure of organization,

- Wages, telephone, electricity, water, etc.