The depreciation can be defined as “the decline in the market value of an asset”.

A machine depreciates (decline in value) because;

– it wears out during usage, and

– no longer possible to perform its functions well as when it was new.

Depending on the type, machinery requires increased maintenance as they age. It reflects a slow and continuing failure of individual parts. In the meantime, the quality and the quantity of outputs may drop due to wear in component parts.

Another feature of depreciation is obsolescence. A machine is termed obsolete when the function it performs can be done in a better manner. A machine may be in excellent working condition, but may still be obsolete. For example, electronic machines, computers, etc.

Value of an asset

Assets always have different values. Those can be termed as the initial value, book value, salvage value, and market value.

The initial value denotes the purchase price of an asset.

Salvage value is the expected selling price of the asset at the end of its useful life.

The book value denotes the current value in the accounting systems. It is equal to the initial value of the asset minus all depreciation costs until the given time. Usually, the book value is calculated at the end of each year.

The market value is the value of the asset when it is sold in the free market. It is not necessary to be equal to the book value.

Depreciation is an accounting method that allows the recovery of the capital cost that was used to procure the asset.

Depreciation – Methods

There are three common methods for calculating depreciation expenses for financial accounting purposes:

- straight-line method,

- sum-of-years digits method, and

- sinking fund method.

Each method involves the distribution of the amount to be depreciated through the recovery life of an asset logically.

Each depreciation method gives a different amount of depreciation expense per period.

The straight-line method assumes linear depreciation. In this method, the depreciation cost is allocated equally over the useful life of the asset.

The sum-of-years digits allocate a high rate of depreciation at the early age of an asset and decreasing rate at its latter stages.

The third, sinking fund method assumes a lower rate at the early life and a faster rate towards the end.

Straight-Line method

The simplest mostly used and best known is the straight-line depreciation method.

In this method, a constant depreciation cost is used throughout the life period of the asset.

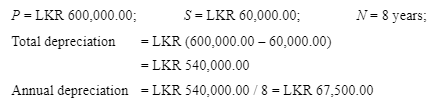

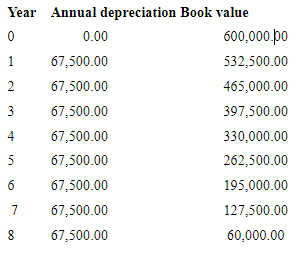

To obtain the annual depreciation cost at any year, Yn, the total value to be depreciated (initial value, P – salvage value, S) is divided by the useful life in the number of years, N.

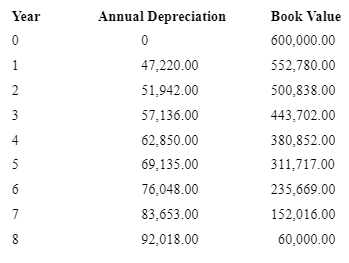

Example 1 – If the purchase price of equipment is LKR 600,000.00 and its salvage value after 8 years is LKR 60,000.00, calculate the annual depreciation and the book value of the equipment each year.

Solution:

Note that the book value of the equipment equals its salvage value at the end of its useful life as shown in the Table below.

Sum-of-years digits method

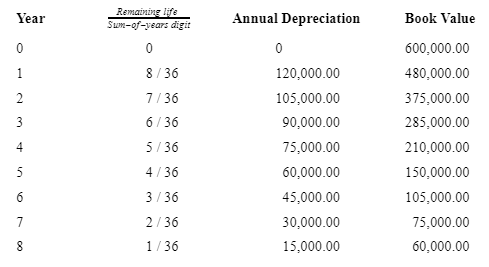

Sum-of-years digit is another method used to allocate the cost of an asset minus its salvage value over its useful life. This method gives faster depreciation at the early stage of the life of an asset resulting in smaller charges as the asset nears the end of its estimated life.

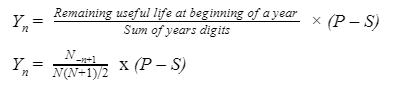

Every year, the depreciation cost is calculated as the remaining useful life at the start of the year divided by the sum of the years digits for the total useful life, with this ratio multiplied by the total amount of depreciation (P – S).

It means the depreciation is calculated as the percentage of the remaining life to the original life.

For an asset with useful life N, to obtain the annual depreciation charge, Yn, at any year n, can be calculated as follows:

Example 2 – Re-calculate the depreciation of the equipment in the above example using the sum-of-years digits method.

Solution –

The calculations are shown in the following table.

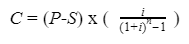

Sinking fund method

This method assumes a uniform series of end-of-payments are paid into an imaginary sinking fund at a given interest rate i.

The amount of the annual payment is calculated so that the accumulated sum at the end of the asset life, and at the stated interest rate, will equal the value of the asset depreciated. (i.e., P -S).

The amount of yearly depreciation is invested in a compound manner for the remaining period as a uniform series of payments using given below:

Then the depreciation value, Yn, at any year n is calculated using the following equation;

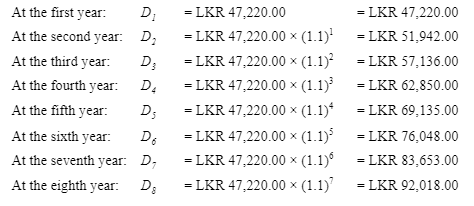

Example 3 – Re-calculate the above example using the sinking fund depreciation method, assuming that the interest rate is 10%.

Solution –

Accordingly, the annual depreciation could be calculated as follows:

The results of the depreciation calculations are summarized in Table below.

After studying depreciation calculations from the above three methods, the depreciated amounts can be summarized as below.

The sum-of-year digits method shows an accelerated depreciation compared to the straight-line method.

The sinking fund is a decelerated method compared with the straight-line method.

However, the straight-line method is the commonly applied and easier calculating method used in asset depreciation.