The construction contractor’s capability to receive contracts and to finish them at a profit is determined by two important factors: cost of people and equipment. To be economically competitive, a contractor’s equipment must be mechanically and technically competitive. Timeworn machines, that require heavy and costly repairs, cannot compete successfully with new equipment having lower repair costs and higher production rates.

In most cases, equipment does not work as a stand-alone unit, pieces of equipment work in groups.

An excavator excavates and loads trucks that haul earth to the filling area on the project. At that point, the earth is dumped and a dozer spreads the material. After spreading, a roller compacts the earth to the required density. Therefore, a group of machines, in this example an excavator, haul trucks, a dozer, and a roller, create what is referred to as an equipment spread.

Optimization in the management of an equipment spread is critical for a contractor, both in achieving a competitive pricing position and in accumulating the corporate operating capital required to finance the expansion of project performance capability.

Equipment cost is often one of a contractor’s largest expense categories, and it is a cost combined with variables and questions. To be successful, equipment owners must carefully analyze and answer two separate cost questions about their machines:

1. What is the cost to be incurred to operate the machine on a project?

2. What are the optimum economic life and the optimum manner to secure a machine?

Elements of ownership cost

Ownership cost is the cumulative cash flows an owner experiences whether or not the machine is productively employed on a job. Most ownership cash flows are expenses (outflows), but a few are cash inflows. The major cash flows affecting ownership cost are;

1. Purchase expense

2. Salvage value

3. Tax savings from depreciation

4. Major repairs and overhauls

5. Insurance

6. Storage and miscellaneous, etc.

Purchase Expense

This is a cash outflow the firm experiences when acquiring ownership of a machine. It is the total purchase expenses. The machine will show as an asset in the firm’s accounting records. The firm has exchanged money, a liquid asset, for a machine, a fixed asset with which the company expects to generate profit.

As the machine is used on projects, wear and tear takes place and the machine can be thought of as being used up or consumed. This reduces the machine’s value because the revenue stream it can generate is likewise reduced.

Salvage Value

Salvage value is the cash inflow a firm receives if a machine still has value at the time of its disposal. This revenue will occur at a future date. However, used equipment prices are difficult to predict. Machine condition, the movement of new machine prices, and the machine’s possible secondary service applications affect the amount an owner can expect to receive.

Tax Savings from Depreciation

The tax savings from depreciation are a phenomenon of the tax system. Depreciating a machine’s loss in value with age will lessen the net cost of machine ownership.

Straight-Line Depreciation

There are several methods for the calculation of depreciation. Straight-line depreciation is one method and it is easy to calculate. The annual amount of depreciation Dn, for any year n, is a constant value, and thus the book value (BVn) decreases at a uniform rate over the useful life of the machine.

Major Repairs and Overhauls

Major repairs and overhauls are included under ownership cost because they result in an extension of a machine’s service life. They can be regarded as an investment in a new machine.

Insurance

Insurance includes the cost to cover fire, theft, and damage to the equipment.

Storage and Miscellaneous

Between jobs or during bad weather, the company will require storage facilities for its equipment. The cost of maintaining storage yards and facilities should be prorated to those machines that require such harborage. Typical expenses include space rental, utilities, and the wages for laborers or watchmen. Usually, these expenses are all combined in an overhead account and then allocated on a proportional basis to the individual machines.

Elements of operating cost

Operating cost is the sum of those expenses an owner experiences by employing a machine on a project. Typical expenses include;

1. Fuel

2. Lubricants, filters, and grease

3. Repairs

4. Tires

5. Replacement of high-wear items

Operator wages are sometimes included under operating costs. When calculating the operator cost, all benefits paid by the company to the operator must be considered.

Fuel

Fuel expense is best determined by measurement on the job. Accurate service records tell the owner how many liters of fuel a machine consumes over what period and under what job conditions. Hourly fuel consumption can then be calculated directly. When company records are not available, the manufacturer’s consumption data can be used to prepare fuel use estimates.

Lubricants

Lube Oils, Filters, and Grease – The cost of lube oils, filters, and grease will depend on the maintenance practices of the company and the conditions of the work location. Some companies follow the machine manufacturer’s guidance concerning periods between lubricant and filter changes. Other companies may follow their own preventive maintenance guidelines.

Repairs

Repairs mean normal maintenance-type repairs. These are the repair expenses incurred on the job site where the machine is operated and would include the costs of parts and labor. Major repairs and overhauls are an ownership cost. Repair expenses increase with machine age.

Tires

Tires for wheel-type equipment are a major operating cost because they have a short life compared to the full lifetime of a machine. Tire costs will include repair and replacement charges. These costs are difficult to estimate because of the variability in tire wear with project site conditions and operator skill.

Replacement of High-Wear Items

The cost of replacing those items that have short service lives compared to machine service life can be a critical operating cost. These items will differ depending on the type of machine, but typical items include cutting edges, ripper tips, bucket teeth, body liners, and cables.

By using either previous experience or manufacturer life estimates, the cost can be calculated and converted to an hourly basis.

Rent and lease considerations

There are three basic methods for acquiring a particular machine to use on a project:

(I) buy (direct ownership),

(2) rent/hire, or

(3) lease.

Each method has inherent advantages and disadvantages.

Ownership guarantees control of machine availability and mechanical condition, but it requires a continuing sequence of projects to pay for the machine. Additionally, ownership may force a company into using obsolete equipment.

Rental / Hire – The rental of a machine is a short-term alternative to direct equipment ownership. With a rental, a company can pick the machine that is exactly suited for the job at hand. This is particularly advantageous if the job is of short duration or if the company does not foresee a continuing need for the particular type of machine. Rentals are beneficial in such situations, even though the rental charges are higher than normal direct ownership expenses. It must be remembered that rental companies only have a limited number of machines and, during the peak work season, all types are not always available. Also, many specialized or custom machines cannot be rented. The principal advantages of hiring a plant on an ‘as and when’ needed basis are that it does not require large sums of capital to be tied up in the plant as well as time devoted to maintenance and storage.

Lease -A lease is a long-term agreement for the use of an asset. It provides an alternative to direct ownership. During the lease period, the leasing company (lessor) owns the equipment, and the user (lessee) pays the owner to use the equipment.

All-in rate for plant

The factors to be considered when calculating an all-in rate for plants are:

- Fixed costs:

- Cost of plant and expected operating life

- Return on capital

- Maintenance costs, and

- Tax and insurance.

- Operating costs:

- Operator’s wages

- Fuel

- Other consumables, including oil, etc.

Fixed costs

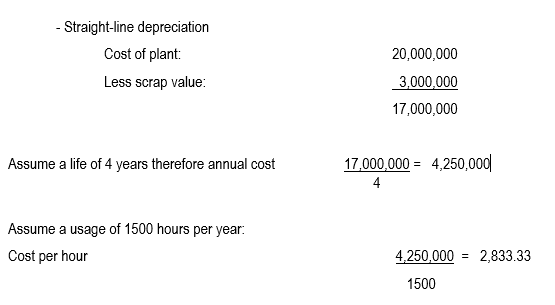

The computation of fixed costs using the straight-line depreciation method is as follows;

Working life

Construction plants come in a variety of types and usually operate in very extreme conditions; however, typical values are as follows:

Concrete mixers 6–7 years

Cranes 8–10 years

Dumper 3–4 years

Excavating plant 5–7 years

Hoists 5–7 years

Lorries 3–5 years

It is usual to assume that a plant works 1500 hours per year. These figures should be used in the calculation of the cost of a plant.

Output

The performance of the construction plant will affect the cost. Therefore, the output or production of a particular item must be known. Once again these statistics are based on historical records.

For example: An excavator fitted with a shovel and having a 0.5 cubic meter bucket will be able to load 12 cubic meters of excavated material into lorries per hour.

A 14/10 (280 liter) concrete mixer will be able to produce an average of 5.0 cubic meters of mixed concrete per hour.

The output/performance of a mechanical plant will be affected by several factors, for example:

• Site conditions, including time of year

• The degree to which plant can be incorporated due to restrictions on site, site organization, etc.

• Skill of the operators.

Plant rates

The following steps can be taken at the tender stage to assess the mechanical plant to be used:

Step 1

Identify specific plants needed by examining quantities and methods. The machine capacities can be found by evaluating the rates of production required. Study the tender programme for overall durations.

Step 2

- Obtain prices; the sources of the plant are:

- Purchase for the contract

- Company-owned plant

- Hire from an external source

- In practice, the sources of prices are:

- Calculate from the first principles

- Internal plant department rates

- Hirers’ quotations

- Published schedules.

Step 3

Compare plant quotations on an equal basis possibly by using a standard form.

Step 4

Calculate the all-in hourly rate for each mechanical plant.

The main parts of the calculation are:

1. Cost of the machine per hour (including depreciation, maintenance, insurance, licenses, and overheads).

2. All-in rate for the operator (the operator may work longer hours than the plant because of the time needed for minor repairs, oiling, and greasing).

3. Fuel and lubricants (the amounts of fuel consumed will depend on the types and sizes of plants; the average consumption during the plant life is used).

4. Sundry consumables (where, for example, the plant specialist is unable to accept the risk of tire replacement on a difficult site or any costs beyond ‘fair wear and tear’).

The cost of bringing the plant to the site is usually dealt with when assessing project overheads (preliminaries) when transporting all plants and equipment.

Step 5

Decide where to price the plant, either in the unit rate against each item of measured work or in the project overheads.

(Plant that serves several trades should be included in the project overheads, such as cranes, hoists, concrete mixers, and materials handling equipment. Estimators also price the erection of a fixed plant in the project overhead with the costs of dismantling the plant on completion).